Bridging Gaps, Changing Lives: Understanding the Impact of Financial Inclusion

To inform its work, strengthen the global evidence base on inclusive finance, and move beyond measuring outputs, SCBF conducts outcome studies with 60 Decibels using their Lean Data methodology. This approach gathers direct feedback from end clients through short, focused surveys, helping to assess changes in clients’ financial health, access to services, and overall well-being. The insights generated, support more effective product design and delivery while guiding SCBF on whereto focus its funding.

In 2024, SCBF initiated a series of outcome studies in partnership with 12 project partners to independently assess the impact of its technical assistance initiatives. By December 2024,seven studies were completed, offering valuable, data-driven insights into how financial services are transforming lives. SCBF conducts these studies to inform its work, validate the impact of the projects it funds, and ensure that financial inclusion efforts effectively meet the needs of underserved communities. These insights provide a deeper understanding of client experiences, financial access, and economic outcomes.

These studies, conducted by 60 Decibels go beyond standard project monitoring to assess the tangible effects of financial services on clients served by SCBF’s partner financial service providers (FSPs). In financial inclusion the gold standard is to design products and services by listening to the voice of clients – through focus groups and other human-centered design approaches. With these studies, we listen to the voice of clients and learn about what works and what doesn’t directly from them. The 60 Decibels methodology employs phone interviews – by local researchers in local languages - that enables rapid data collection and analysis. Each study represents interviews with a randomized selection of around 275 clients. Through the interviews, we collected quantitative and qualitative data allowing us to examine client profiles—gender, income levels, geographic distribution, and household size—as well as improvements in financial access, income, savings, and overall well-being.

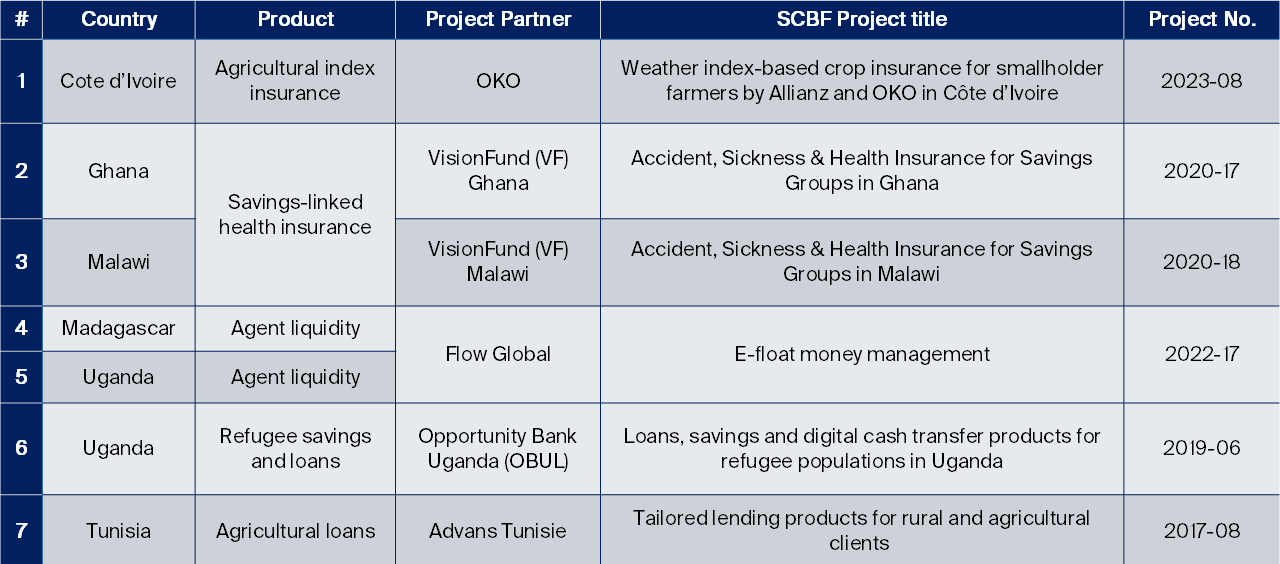

The first set of studies focused on a diverse range of financial products and services designed to meet the needs of low-income and underserved populations:

Project No:2023-08 - Factsheet ; Final Report ; Outcome study

Project No:2020-17 - Factsheet ; Final Report ; Outcome study

Project No:2020-18 - Factsheet ; Final Report ; Outcome study

Project No:2022-17 - Factsheet ; Final Report ; Outcome study - Madagascar ; Outcome study - Uganda

Project No:2019-06 - Factsheet ; Final Report ; Outcome study

Project No:2017-08 - Factsheet ; Final Report ; Outcome study

By evaluating these products across different markets, the studies provide crucial insights into how financial inclusion efforts translate into meaningful change for individuals, families, and communities.

Who Are the Clients benefiting from these projects?

A clear picture of the clients benefiting from these financial services is emerging. Across the different products and services examined (not necessarily representative of SCBF’s project portfolio), several key trends stand out:

> Income: SCBF’s projects specifically target vulnerable populations, ensuring that financial services reach those who need them most. Most clients served by SCBF partner FSPs live below the national poverty line of $3.65 per day:

This data reinforces the importance of financial inclusion initiatives that prioritize the most economically vulnerable communities.

> Location: Most clients live in rural areas, with between 62% and 93% residing outside urban centres. The exception is agent liquidity services, which are used more often in urban and peri-urban settings due to the nature of mobile money transactions and agent-based banking.

> Household Size: Clients in Sub-Saharan Africa tend to have larger households, averaging between 6 and 9 people per household, reflecting broader regional trends

> Gender: On average, 42% of the survey respondents are female, while 58% are male. However, participation varies by product type.

- Agricultural loans and insurance are dominated by male clients (89-95%), reflecting broader gender dynamics in smallholder farming.

- Agent liquidity services and savings-linked health insurance have higher female participation (59-73%), as these models—such as Village Savings and Loan Associations (VSLAs)—are often designed to support women.

This data aligns with project reporting to SCBF with a 57% outreach to female clients.

> Age: The typical SCBF-supported client is between 42 and 44 years old, except for users of agent liquidity solutions, who tend to be younger, averaging 32 years old. This suggests that financial service providers (FSPs) often attract middle-aged clients with stable income-generating activities, while newer digital-based solutions like agent liquidity appeal to younger entrepreneurs.

How Financial Services Improve Lives - Access as a Catalyst for Change

For many clients, financial services are not just an improvement but a first-time opportunity. Across all products, an average of 76% of clients had never accessed a similar financial service before. First-time access rates ranged from 53% to 96%,depending on the product and the maturity of the financial services market.

Products like agricultural insurance and agent liquidity solutions, which are relatively new in many regions, had particularly high first-time access rates. Without these services, many clients reported that they would have had to rely on informal lending from family and friends—or, in some cases, go without financial support entirely.

The studies provide strong evidence that financial access translates into meaningful improvements in income, savings, and overall well-being.

Transparency and Customer Satisfaction

The customer service and transparency of FSPs in their terms and pricing can be equally as important as the actual financial product. Overall survey respondents from all studies reported the terms and conditions were easy to understand across products with scores ranging from 72% to 93%. Further reinforcing the positive outcomes reported by clients. In all the studies, approximately 40% of clients reported satisfaction levels indicating they would recommend the product or service to family and friends.

Insights from thematic project areas

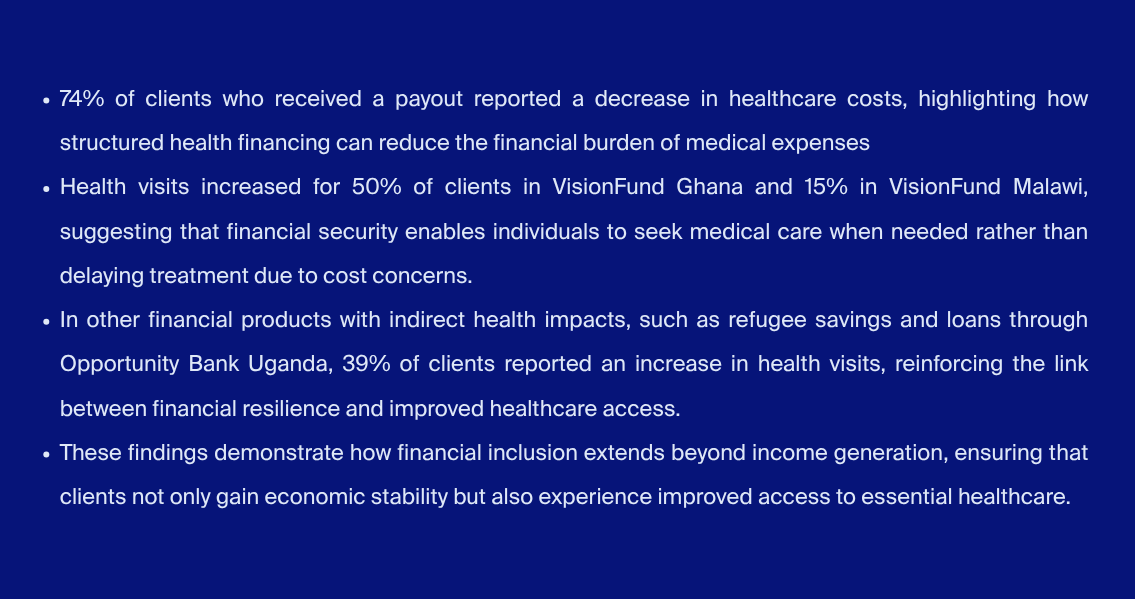

Health – Clients reduce out-of-pocket expenses and improve access to healthcare

Beyond financial stability, access to tailored financial products also contribute to improved health outcomes. The studies reveal that among clients of savings-linked health insurance provided by VisionFund Ghana and VisionFund Malawi:

Agriculture - Smallholder farmers increase investment, productivity, and resilience

For many low-income households, agriculture is the backbone of economic stability. Access to financial products such as agricultural loans and insurance enables farmers to invest in their livelihoods, enhance productivity, and build resilience against economic shocks.

Findings from the studies of agricultural insurance (OKO Cote d'Ivoire) and agricultural loans(Advans Tunisie) reveal the following:

These findings emphasize the transformative impact of financial services in agriculture - helping farmers plan ahead, increase productivity, diversify income sources, and invest in their families' futures.

Migration - Displaced persons build economic stability, reduce financial stress and improve resilience

Refugees fleeing civil unrest and conflict zones in their home countries are often displaced indefinitely. Asa result, they often lose their social and economic support systems and need to rebuild their lives from zero. Access to tailored financial products and services that lower the barriers to entry, can transform the lives of refugees, offering them the opportunity to rebuild and positively contribute to their host communities and economies.

A study on refugee savings and loans with Opportunity Bank Uganda (OBUL) highlighted the transformative impact of these financial services:

These findings demonstrate how targeted financial services, and support can empower refugees to build more stable, resilient futures while contributing to the broader economic and social fabric of their host communities.

Conclusions

The outcome studies conducted with 60 Decibels provide compelling evidence of the transformative impact of financial inclusion on underserved communities of projects funded by SCBF. By capturing direct client feedback, SCBF has gained critical insights into how financial services are improving income, savings, and overall well-being. The data highlights not only increased financial security but also broader benefits, such as improved healthcare access, enhanced agricultural productivity, and greater resilience among refugee populations. These findings reinforce the value of SCBF’s approach to funding client-centric financial products and services, ensuring that financial inclusion efforts are both impactful and responsive to the needs of vulnerable communities.

What’s Next?

The findings from these studies affirm the significant, positive impact of financial inclusion. However, there is still work to be done to:

- Expand gender-inclusive financial services by designing products that align with local economic and cultural dynamics.

- Continue developing products that cater to rural populations, ensuring that financial solutions reach those with the greatest need.

- Strengthen savings and resilience-focused products to help clients build long-term financial security.

SCBF is committed to advancing financial inclusion and will complete sixteen additional outcome studies in 2025. These studies will provide a more comprehensive understanding of the impact of SCBF’s support for financial service providers, enabling a more data-driven approach to enhancing and scaling inclusive financial solutions. When financial services are designed with inclusivity in mind, they don’t just improve numbers - they transform futures.

.png)

.png)

.png)

.png)