Closing the Protection Gap: Insights on emerging customer-centric approaches and public-private partnerships from our new member AXA

The AXA Group is a worldwide leader in insurance and asset management, serving 105 million clients in 54 countries. As one of the largest global insurers, their purpose is to act for human progress by protecting what matters. AXA empowers people to live a better life by providing them the confidence of quality safety nets in case something happens. Still today, a large part of the world population remains excluded from traditional insurance due to cost, access, understanding or trust. AXA Emerging Customers was set up in 2016 to address these issues and expand AXA’s footprint by providing tailored solutions for this vastly un(der)served low income to mass market segment.

In November 2021, we welcomed AXA as SCBF’s 27th member. We spoke with Garance Wattez-Richard, Head of AXA Emerging Customers, to learn more about their work and how our new partnership can help bridge the protection gap for financial inclusion

What challenges is AXA aiming to solve through the Emerging Customers portfolio? Why emerging customers instead of emerging markets?

AXA Emerging Customers aims to accompany low to middle income households on their economic progression and provides protection solutions that prevent them from falling into poverty.

Since inception, we have put human-centered design as a core driver of our business. Today, our customers are people from low to mass-market segments with volatile income and limited social protection, who boost their financial resilience and living standard through our inclusive insurance schemes. Why ‘Emerging Customers’? Because they are present throughout the globe, although the challenges at stake are different: in emerging markets the middle class is growing as people rise out of poverty while in countries like France the lower end of the middle class is faced with a growing risk of sliding downwards.

In your experience, what type of insurance products are most in demand in emerging markets?

Our product approach initially focused on top-of-mind threats like health, accidents and protection of basic property. We are now broadening our range of services with a specific focus on health services and agriculture, by providing simple, efficient, and customer-oriented products. In addition, factors such as new technologies, digitalisation and COVID-19 have also tremendously affected the demand for innovative and accessible insurance solutions. Examples include telemedicine and digital health advisory service as part of the health insurance offering, and index-based insurance in agriculture.

If you had access to all the required resources and partnerships, what would you prioritize in the quest to close the insurance gap/protection gap?

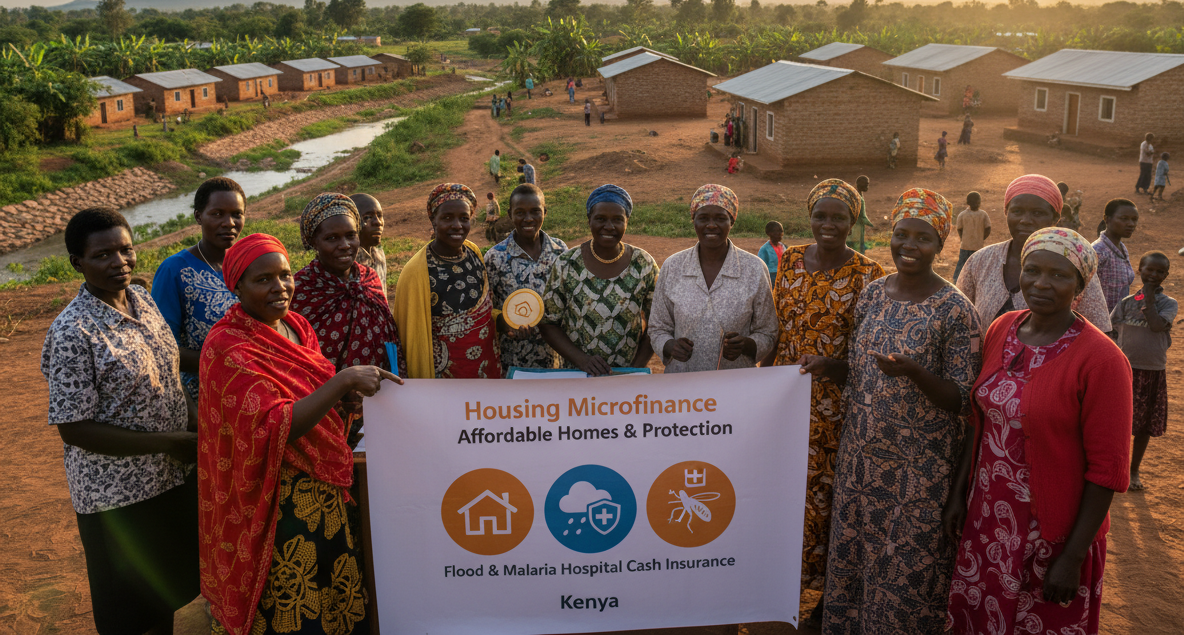

Four in five people in most emerging markets have never had insurance. The task at hand is daunting, especially when it comes to building safety nets to achieve universal healthcare coverage and enhancing the climate resilience of farmers.

My dream would be to build effective public-private partnerships to tackle these issues. Platforms like the Insurance Development Forum (IDF) have managed to unite the insurance industry with multilaterals such as the World Bank or the United Nations Development Programme to build resilience against climate change. If I had a magic wand, I would want to expand the logic towards covering other essential risks such as life and health, by partnering with similar actors but most importantly local governments. Today, when the main bread-earner of a low-to-middle income family in India, for example, dies, the entire family falls economically, sometimes as far down as poverty. What if we invented a scheme to provide two years’ worth of income to any family experiencing this tragedy? By sharing the risk, leveraging economies of scale and riding on existing government channels serving these populations, we could have huge impact.

How is AXA prioritising/addressing gender inequalities?

AXA worked with the IFC and Accenture to analyse the role of the insurance industry in reducing the protection gap for women. AXA also has a Women in Insurance Initiative and through AXA Emerging Customers we have already executed several projects that exclusively protect women in countries like Egypt and Burkina Faso.

We integrate gender-sensitive approaches in our development strategies to empower women and strengthen their resilience. What we have learned is that women are an effective conduit to the holistic protection of their household, but also that we need to accompany their growing professional responsibilities. Often these aspects overlap, which is why with tailored covers we can protect their income, for example, when they have to bring children to the hospital and close the shop for the day. The role of women differs quite a lot by country and often within different regions of a country, which is why any approach needs to be locally tested with the end beneficiaries. The road to Hell is paved with good intentions, as the saying goes.

Why SCBF? What drove your decision to join us as a member?

Like AXA Emerging Customers, SCBF is striving to enhance the quality of life for vulnerable people by supporting innovative financial solutions. Building resilience, boosting economic empowerment, and evaluating essential services to enrich the living standards of this segment are the main objectives of SCBF, which strongly resonate with our purpose. We are therefore delighted to join because we believe it is one of the smart and agile public-private initiatives in the space, one that doesn’t oppose the public and the private sector rationales but tries to bring the best of both worlds together, with the overarching ambition of contributing to sustainable development.

How do you see this partnership with SCBF bringing AXA closer to its ambition of protecting emerging customers from risks so they can thrive? What would be a measure of success?

Strategic collaborations are crucial to our success. Sharing mutual vision and integrity, our partnership will not only facilitate inclusive insurance in the emerging world but will also help us to move forward towards our objective of “going beyond pure insurance towards more holistic financial protection of our customers”. Therefore, our measure of success will be the ability to scale and replicate offers based on evolving and more adapted operating models.

As we embark on this partnership, what are you most excited about doing with us in the coming months?

Innovating financial inclusion! There are a lot of exciting initiatives happening in the field and by combining public and private sector assets, we have the opportunity to have a greater impact. For example, our upcoming collaboration to combine health insurance with money transfers to protect the migrant workers’ families back home holds great promise, and we hope we can take it forward despite the current travel constraints.

Garance is CEO of AXA Emerging Customers, a business she founded in 2016 that aims to protect the un(der)served populations, from low to middle income, across emerging markets - and increasingly in mature ones. She has been working for AXA in a variety of capacities, ranging from Executive Assistant to the AXA IM CEO, to Global head of AXA IM Research Marketing and AXA Group Head of External Communications. Amongst other initiatives, she launched the SheForShield report in partnership with the IFC & Accenture, the first industry report of its kind to highlight the significant opportunity for the insurance industry of better protecting women, across income brackets and geographies. She previously worked for strategy consultancies and multilateral organisations.

She holds a BA in Finance and Management from Université Paris IX Dauphine (MSG), an MSc in Economics and International Relations from the London School of Economics (LSE - MSc Politics of the World Economy), another from Sciences PO Paris in Economics (DEA Economie Appliquée) and an MBA from INSEAD. She sits on the Boards of AXA France, Bharti AXA Life in India and Baobab (ex-MicroCred).

Garance is the winner of the first Women in Insurance Award of the Geneva Association, and is a Schwab Foundation Social Innovation awardee.

If you are interested in becoming an SCBF Member, please write to us at info@scbf.ch.

Photo credits: AXA

.png)

.png)

.png)

.png)